Valuing an Agency Business: A Comprehensive Guide

Introduction

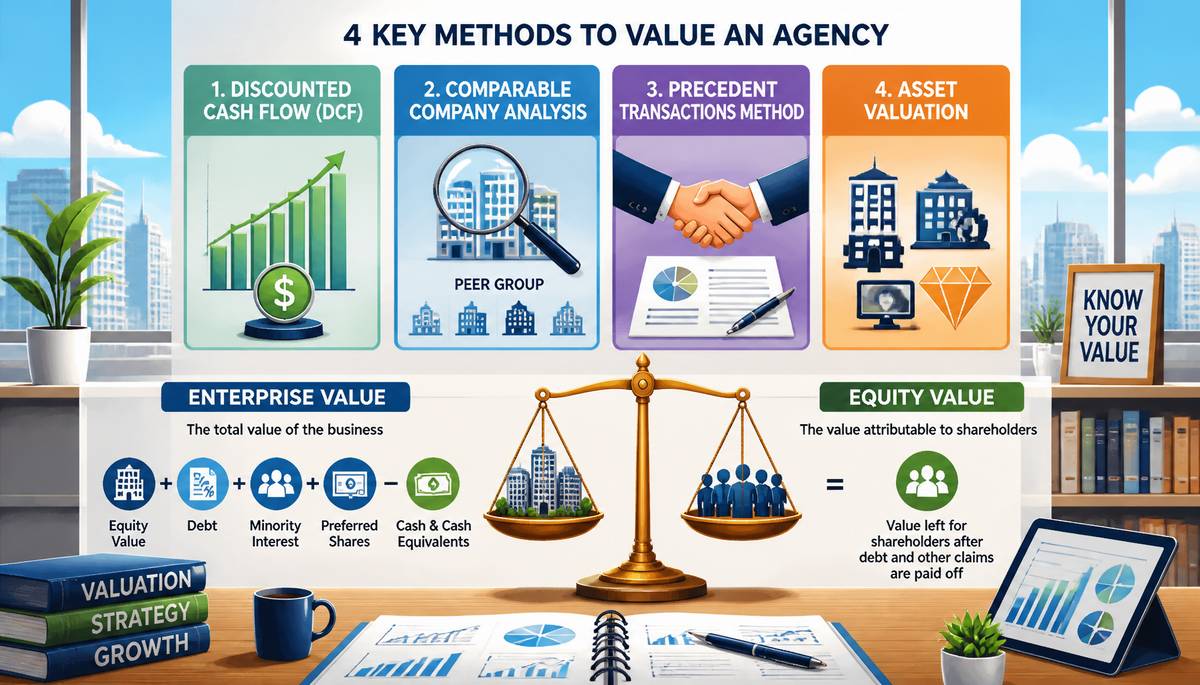

Understanding the value of your agency business is essential for many reasons, from merger and acquisition considerations to partnership buy-ins and buy-outs, to succession planning. This blog post will delve into the four key methods used for valuing an agency: Discounted Cash Flow (DCF) valuation, comparable company analysis, precedent transactions method, and Asset valuation.

Discounted Cash Flow (DCF) Valuation

The DCF method of valuation is based on the future cash flows that the business is expected to generate. These projected cash flows are then "discounted" back to the present day to provide a present value estimate. The DCF method is arguably the most detailed valuation tool, as it considers future business performance and the risk of achieving predicted cash flows.

Comparable Company Analysis

Comparable Company Analysis, often referred to as "trading multiples" approach or ā?opeer groupā?¯ analysis, is a valuation method that involves comparing the current value of your agency to similar businesses in your industry or sector. This method uses various financial metrics such as Price-to-Earnings (P/E), Enterprise Value-to-EBITDA (EV/EBITDA), and others. The key to this method is finding a 'peer group', a set of businesses similar to yours in terms of size, growth, risk, and profitability. Once the 'peer group' is established and trading multiples are calculated, these ratios are applied to your agency's financial metrics to estimate a value. This method provides an industry context and can offer a reasonable value range for your agency. However, remember that every business is unique, and factors beyond the financials may impact the final valuation. It's important to consider these elements to ensure an accurate and comprehensive valuation of your agency business.

Precedent Transactions Method

The Precedent Transactions Method is somewhat similar to Comparable Company Analysis, but instead of looking at similar businesses that are currently trading, it looks at similar businesses that have been sold recently. By understanding how much a buyer was willing to pay for a similar business, we can infer what they might be willing to pay for our agency.

Asset Valuation

Asset Valuation is an approach that ascertains an agency's worth based on the total value of its tangible and intangible assets. For agencies that possess substantial tangible assets such as infrastructure, property, or equipment, this method can render an approximate minimum value. However, for many agencies, substantial value is embedded in intangible assets like brand value, customer relationships, proprietary technology, and intellectual property. In these instances, it's crucial to adopt methods that can accurately estimate the present and future worth of these assets. Notably, Asset Valuation is rarely used in isolation. Instead, it often complements other valuation methods, such as the Discounted Cash Flow or Precedent Transactions Method, providing a more expansive and balanced view of a company's value. Remember, every agency is unique, and the Asset Valuation method should be adapted appropriately to account for these individual characteristics.

In conclusion, valuing an agency business can be a complex process with many considerations. It is important to understand and analyze these different methods to get a comprehensive understanding of your business's value. Remember that these methods do not operate in isolation and it is often beneficial to use a combination of these techniques to arrive at a more holistic valuation.

If you're interested in learning more, we recommend this resource for more information:

https://kimberlyadvisors.com/articles/intro-to-private-company-valuation

Enterprise Value vs Equity Value

Understanding the distinction between enterprise value and equity value is crucial in the sphere of business valuation. At the most basic level, enterprise value provides an accurate valuation of a company's entire worth, while equity value represents the portion of that worth attributable to shareholders.

Enterprise value, often referred to as firm value, encapsulates the total value of a business. It considers not only the equity (shareholders' value), but also the company's outstanding debt, minority interest, and preferred shares, while subtracting any cash and cash equivalents. This holistic approach makes enterprise value a particularly useful metric in mergers and acquisitions, as it encapsulates the entire picture of a businessā?Ts value, beyond just the equity or market capitalization.

Equity value, on the other hand, is the value left for the equity shareholders after debentures, loans, and preference shares are paid off. Simply put, it is the market capitalization of the company. Equity value is important for shareholders as it indicates the portion of a company's value that they can actually claim.

DCF (Discounted Cash Flow) valuation provides us with the enterprise value of a company when it uses the unlevered free cash flows and discounts them back in time at their weighted average cost of capital (WACC). Unlevered free cash flows are the cash flows available to the firm's investors, both debt and equity. WACC is the average rate of return a company is expected to provide to all its security holders to justify the risk. In essence, DCF valuation offers a measure of the intrinsic value of an entire business, giving us the enterprise value.

It's crucial to differentiate between these concepts when evaluating a business's worth. While both enterprise value and equity value offer valuable insights, they serve different purposes and should be applied accordingly.

To learn more, about this point, you can use this as a reference:

https://kimberlyadvisors.com/articles/enterprise-vs-equity-value

|

|